AI provider selection in 2026: ChatGPT drops below 50 % — what SMEs need to know

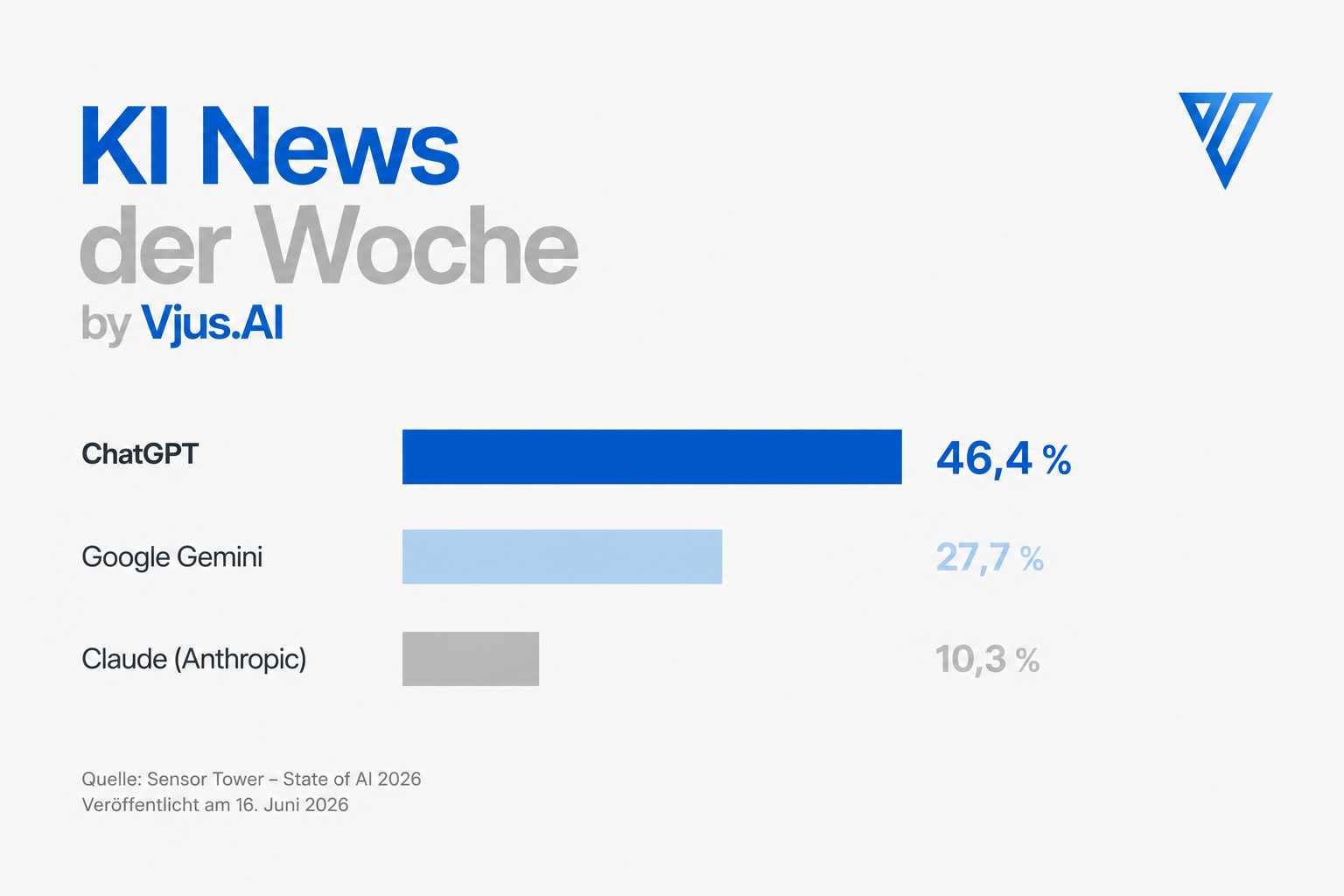

For the first time, ChatGPT holds less than half the global AI assistant market. The Sensor Tower State of AI 2026 report puts it at 46.4 %, with Gemini at 27.7 % and Claude at 10.3 %. For SMEs evaluating AI tools, this fragmentation creates both opportunity and new decision complexity — here is how to navigate it.

For years, the question of which AI tool to use was straightforward for most companies: ChatGPT. That is changing. According to the Sensor Tower State of AI 2026 report, published on 16 June 2026, the ChatGPT share of global AI assistant users has for the first time fallen below 50 per cent — to 46.4 per cent. Google Gemini now holds 27.7 per cent of the market, and Claude by Anthropic 10.3 per cent. For companies that are starting to use AI now, or reconsidering their current tool choice, this is a meaningful development.

The numbers behind the shift

In absolute terms, ChatGPT remains dominant: 1.1 billion monthly active users, versus 662 million for Gemini and 245 million for Claude. But the direction matters more than the current position. ChatGPT held over 50 per cent of the market as recently as January 2026, by May it had slipped below that threshold for the first time. The overall market is expanding rapidly: spending on AI assistants in the first half of 2026 reached 4.2 billion US dollars, more than double the 1.83 billion in the same period of 2025. This means competitors are gaining share in a growing market — not on the back of a shrinking one.

What is driving users to switch

The Sensor Tower data points to two specific events that accelerated movement away from ChatGPT. First, the OpenAI contract with the US Department of Defense, announced in February 2026, triggered a 295 per cent spike in uninstalls. Second, OpenAI began introducing advertising: by May 2026, 17 per cent of daily active ChatGPT users were being shown ads in the application. The data shows that brand trust and values alignment are now factors in tool selection, not just feature sets. Claude illustrates this concretely: 13 per cent of its users pay for a subscription — the highest conversion rate in the field — pointing to a user base that is actively integrating the tool into work processes rather than using it occasionally.

What this means for mid-sized companies

The fragmentation of the AI assistant market is good news for companies evaluating their options: serious alternatives exist, competition is pushing quality up and prices in a more favourable direction. At the same time, the decision is no longer obvious. Any company evaluating a KI tool for internal use — whether for text work, process automation or customer communication — faces more options and more decision complexity. A structured technology evaluation turns that complexity into a documented decision with clear criteria, rather than a guess based on which brand is loudest.

- Use case first: which specific tasks should the AI tool take over — text drafting, data analysis, customer communication, coding assistance? Different models have different strengths; benchmark rankings rarely translate directly to a specific business task.

- Data protection and hosting: where is the data processed — in the EU or the US? For companies in regulated sectors, or those handling personal data, this question must be answered before signing a licence, not after.

- True cost of adoption: flat rate, per-token pricing or enterprise licence? The monthly subscription is only part of the picture; integration effort, onboarding and change management are often a larger investment.

- Vendor dependency: what happens if the provider raises prices, changes its terms of service, or goes offline due to regulatory decisions — as happened with Fable 5 for two weeks in June 2026? A AI integration strategy built on a single provider creates a concentration risk that is easy to underestimate.

How to approach the selection in practice

The starting point for most mid-sized companies without a large IT department is a pilot on a single, clearly scoped use case — not a platform decision for the whole company. Pick the task where the productivity gain is most measurable: a specific type of document, a recurring analysis, a customer-facing FAQ. Run it for four to six weeks with one or two tools and use the result to inform the broader decision. This kind of focused pilot can be set up and evaluated as part of a structured IT consulting engagement in a few weeks, without committing to a multi-year enterprise contract upfront.

The AI market has stopped being a one-provider race. Companies that stay informed and keep their options open will make better decisions — and avoid expensive lock-in.

Verdict: what to do now

For companies that have not yet systematically evaluated AI tools: conditions are currently favourable. Prices are competitive, alternatives are available, and the tools are mature enough for real business use. Start with one concrete use case, document the result and decide from evidence rather than marketing claims. For companies already using ChatGPT: no immediate action needed, but review your data protection agreements and know your exit options. For companies with elevated data protection requirements — regulated industries, personal data, sensitive business information: the question of where and how data is processed is non-negotiable. Involve your data protection officer or an experienced IT consulting partner before expanding AI use across the organisation.